From 'V2G capable' to dispatchable — the five gates in between

The complete map of what registration, communication, metering, hardware, and aggregation actually require before the UK grid pays your V2G asset

The UK has one consumer V2G tariff open to new customers. It supports four cars. The queue of vehicles described as “bidirectional”, “V2G-capable”, or “vehicle-to-grid ready” stretches considerably further.

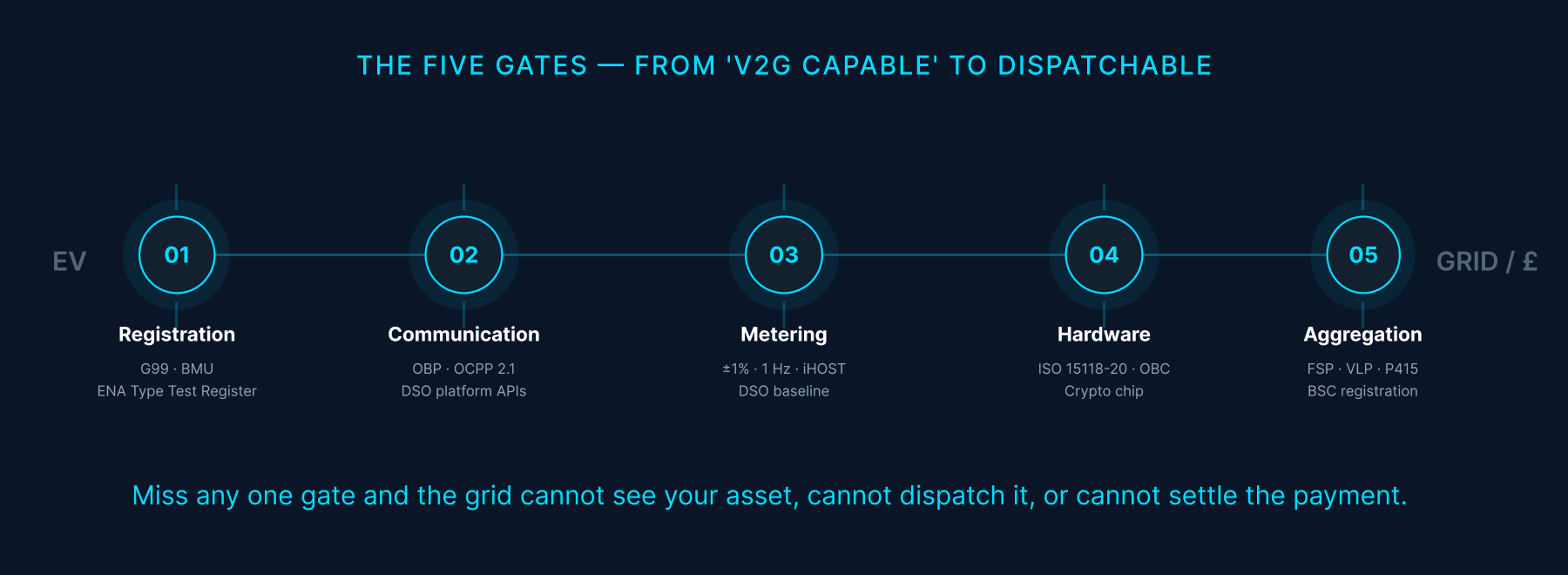

That gap exists for several reasons — and hardware is one of them. Some of the vehicles the industry calls V2G-capable have not been certified for UK grid export. Some chargers lack the response speed or metering precision the grid requires. But hardware is only one gate. Between a V2G-capable vehicle and a grid payment sit five gates that most of the industry has never seen mapped end to end: registration, communication, metering, hardware, and the commercial layer that connects your asset to a paying market. Miss any one of them and the grid cannot see your asset, cannot dispatch it, or cannot settle the payment.

This article maps those five gates.

Inside the UK electricity market’s four layers covered four markets where flexibility earns money in Great Britain: the Capacity Market, wholesale trading, the Balancing Mechanism, and ancillary services (Dynamic Containment, Quick Reserve, Slow Reserve). I left out a fifth — DSO local flex — deliberately. DSO markets are operated by Distribution Network Operators at distribution voltage, under rules that are distinct from NESO’s national framework.

This article is written for three audiences, each asking a different question about the same problem:

Fleet operators: Which vehicles and chargers are eligible for UK grid payments today, which markets can they access, and what do you register with whom?

Charge point operators (CPOs): What communication protocols, metering hardware, and market roles does your infrastructure need to participate in grid services?

Charger and vehicle manufacturers: What specifically needs to change in your hardware, firmware, or software to unlock each market — and what kind of change is it?

Navigating this article: Fleet operators: Gates one and five are your immediate priorities. CPOs: Gate two (communication) and Gate three (metering); Gate four provides useful context. Charger and vehicle manufacturers: Gate four is written with you in mind; Gates one and three give the regulatory and metering context.

Latest articles:

If you haven’t subscribed yet, here’s what was covered in the past weeks:

One UK tariff, four vehicles — the real state of V2G in 2026

As of June 2026, the only consumer V2G tariff open to new sign-ups in the UK is the Octopus Power Pack, which launched in February 2024. It supports exactly two vehicle and charger combinations:

BYD Dolphin with a Zaptec Pro charger (AC bidirectional, CCS2)

Nissan Leaf (older model), Nissan e-NV200, or Mitsubishi Outlander PHEV, each with a Wallbox Quasar 1 (DC bidirectional, CHAdeMO)

That is it. One open tariff. Four compatible vehicles. Two charger types.

A small number of OVO Energy Project Sciurus participants — those with an Indra bidirectional charger and a Nissan LEAF with a 30 kWh or larger battery — have been migrated by Indra to a production-ready V2G platform powered by Kaluza. Indra describes this as commercially deployable and live with real customers today — but the pathway is not open to new sign-ups. OVO’s V2G product page describes the company as “currently preparing for the next phase of V2G”, and its published export rates have not been updated since March 2023.

For practical purposes, the UK’s commercial V2G market for new entrants is Octopus Power Pack.

Octopus states savings of £620 per year compared to standard variable rates (assuming 7,500 miles annually at an average rate of 0.306 kWh/mile). To qualify, you need

a compatible vehicle and charger,

a smart electricity meter,

a G99 certificate from your Distribution Network Operator, and

the ability to plug in for at least 12 hours a day on at least 20 days per month.

The G99 certificate is where most conversations about V2G confuse people. It is essentially a planning permission for your charger to export electricity to the local network. Without it, a V2G charger is legally prohibited from sending a single watt back to the grid, regardless of what its datasheet says. We will come back to G99.

A note on three letters that are frequently conflated: V2L, V2H, and V2G are not the same thing.

V2L (Vehicle-to-Load) powers devices from a socket in the car — a camping extension lead, a power tool on a building site. It does not interact with the grid.

V2H (Vehicle-to-Home) powers your house when the grid is unavailable. It also does not interact with the grid.

V2G (Vehicle-to-Grid) exports electricity to the distribution network and receives payment for doing so. This is what the markets mentioned in my previous article buy.

Most of the bidirectional capability announced by manufacturers in 2024 and 2025 is V2L or V2H — genuinely useful, but not the same as getting paid by the grid. The Hyundai IONIQ 5 and Kia EV6’s bidirectional features are V2L. Where genuine V2G exists, it tends to be market-specific: Tesla Powershare (Cybertruck only, not sold in the UK) does V2G in the US — the Cybertruck (123 kWh of capacity) launched V2G in Texas in February 2026 and was approved for PG&E’s residential V2G pilot in California in April 2026 — but the Cybertruck is not sold here. The VW ID.3 home kit is V2G — but only in Germany. The Renault 5 E-Tech does V2G in France; UK deployment has been stated for 2026 but is not yet live.

Hyundai Motor Group and Vattenfall announced in May 2026 a six-month V2G field trial in the Netherlands — up to 80 private households, each receiving a bidirectional charger, with the Kia EV9 or Hyundai IONIQ 9. Participants can return electricity to the grid between 4pm and 9pm when demand peaks, and Vattenfall reimburses home charging costs up to €500 over the six months. The vehicles matter here: unlike the IONIQ 5 and EV6 whose bidirectional capability is V2L, the EV9 and IONIQ 9 target genuine grid export. That the Netherlands already has commercial V2G — 220 Renault EVs in Utrecht are earning revenue from grid services today — does not make this a redundant trial. V2G compliance is vehicle- and market-specific; the EV9 and IONIQ 9 have not been certified against Dutch grid codes. The field trial is how that certification evidence gets generated.

The UK has its own version of that certification bottleneck — and in one region, it is getting faster. UK Power Networks became the first Distribution Network Operator to automatically approve V2G connections, in March 2026. UKPN now approves approximately 80% of low-carbon technology applications instantly — compared to a national average of 11%. The technical condition is that the device must be type-tested and listed on the Energy Networks Association Type Test Register. For UKPN customers using listed equipment, a process that previously took months now takes seconds.

The ENA Type Test Register is the Energy Networks Association’s authoritative list of generation and export equipment that has been type-tested to G98/G99 standards. It is not a government list of “approved V2G vehicles” but it is the closest thing the UK has to one, and it is the gating database for all DNO connection approvals. Being on this register is what enables UKPN’s automatic approval.

As of 31 May 2026, the register lists eight compliant V2G inverter entries from five organisations: Octopus Energy, Nissan, Indra Renewable Technologies, ABB, and PRE Power Developers. The Indra Smart PRO — a 6 kW DC bidirectional charger — is a purchasable product, but there is no open consumer tariff to connect it to for new customers in 2026. The ABB entry is a three-phase commercial charger deployed through a vehicle-to-grid programme in France. Type approval is a prerequisite for grid connection. It does not come with a tariff attached.

")

The five markets — and which ones V2G can reach today

The previous article covered four national markets operated by NESO. There is a fifth, distinct from them:

DSO local flex is operated by Distribution System Operators (DSOs) at distribution voltage — separate from anything NESO (National Energy System Operator) manages.

DSO vs DNO: A note on terminology that the industry uses inconsistently: in Great Britain, the same six companies that operate as Distribution Network Operators (DNOs) — the licensed entities that own the local wires and connect customers — also fulfil the DSO role when they run flexibility markets and procure grid services from distributed assets. “DNO” refers to their regulated network function; “DSO” to their active market role. Same organisation, two hats.

Six major DSOs cover Great Britain:

UK Power Networks (UKPN),

National Grid Electricity Distribution (NGED),

SP Energy Networks (SPEN),

Electricity North West (ENW),

Northern Powergrid, and

Scottish and Southern Electricity Networks (SSEN).

Each operates its own flexibility market with its own rules and pricing. Platforms include Piclo Flex, Local Flex, Electron Connect, and Market Gateway. The total contracted across DSO markets was approximately 9 GW in 2025 (published October 2025), making it the world’s largest local flexibility market according to the authors. They project £3bn in savings by 2028 through avoiding or deferring network reinforcements, reducing connection charges, and increasing the use of low-carbon energy sources. Given that the Clean Power 2030 Action Plan has outlined a system-wide flexibility requirement of 51-66GW by 2030, the local flexibility market is a significant puzzle piece to turn this plan into reality.

For EV fleets connected at distribution voltage — which is most of them — this market is the most immediately accessible. For a detailed walkthrough of how DSO flexibility markets actually work — from tender design and bid assessment through to dispatch, measurement, and settlement — I can recommend Blake Clough Consulting’s guide to GB DSO flexibility markets.

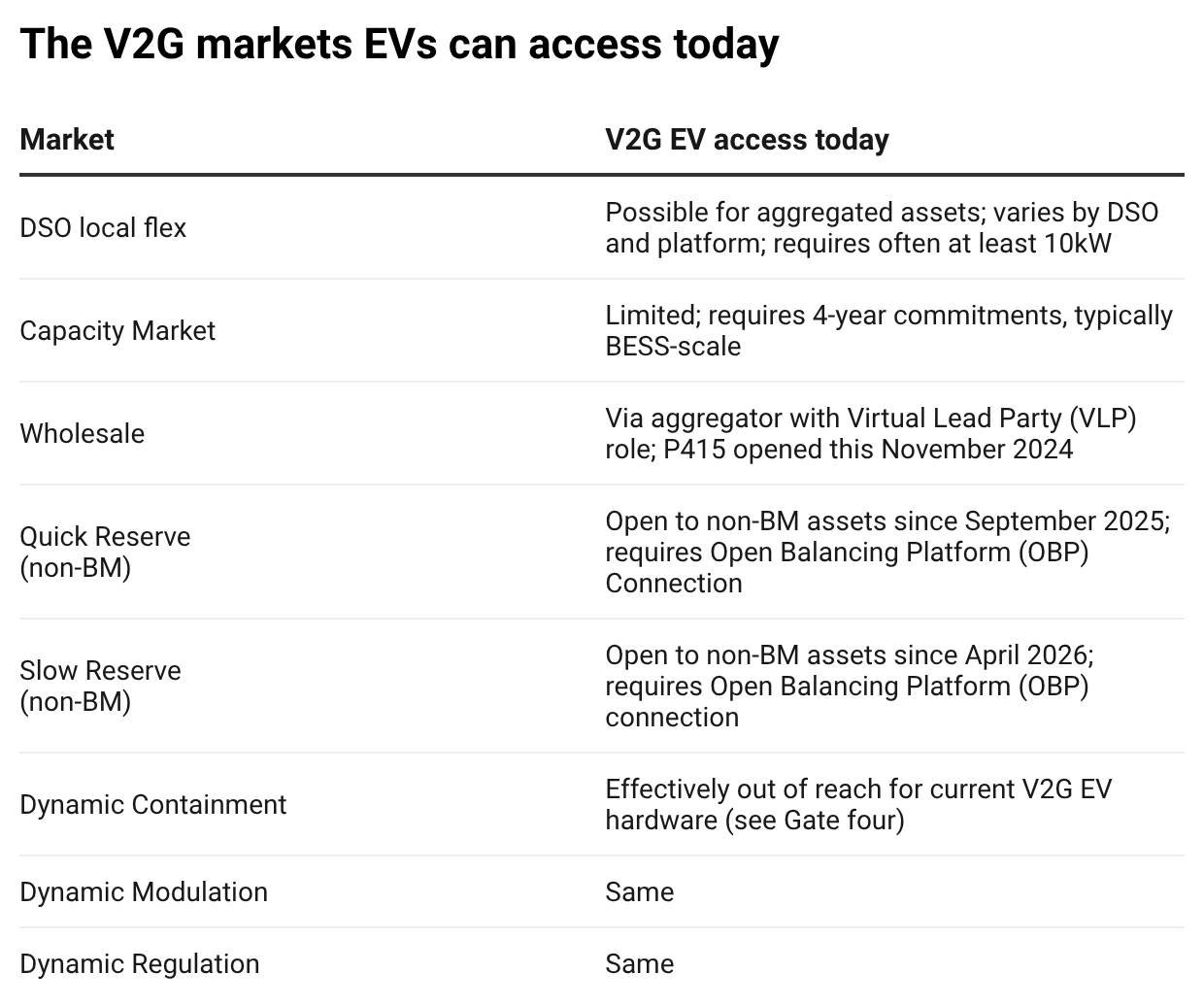

Here is the honest picture of which markets V2G EVs can access today in the UK:

The reasons for that last row require understanding the metering and hardware stacks. We will get there. Now let’s shed light onto the five gates you need to tackle to turn your asset from ‘V2G capable’ to dispatchable.

Gate one: registration — your asset needs an identity

Before any market will accept your asset, you need to register it. What you register with depends on which market you are entering.

For NESO-operated markets (the Balancing Mechanism and all ancillary services), your asset must be registered as a Balancing Mechanism Unit (BMU) with NESO. A BMU is NESO’s unit of account for market participation — the identifier against which physical notifications, dispatch instructions, and settlement calculations are attached.

Think of BMU registration as opening a bank account. Without it, nobody can pay you for grid services. The Balancing and Settlement Code (BSC) is the rulebook governing what the account can be used for. Elexon administers the BSC and runs the settlement system. NESO operates the market.

To be registered as a BMU, you also need an electricity Supplier as the counterpart, because the BSC framework assumes every generation or consumption unit is associated with a supply arrangement. This is where aggregators — and a specific BSC role called the Virtual Lead Party (VLP) — become relevant.

For DNO connection approval, you need a G99 certificate. The first UK G99 AC V2G certification was issued to Nissan Motor Co. by TÜV Rheinland on 19 November 2024. This was notable specifically because it was AC-based — CHAdeMO-based DC V2G (the Wallbox Quasar 1 pathway) had existing certifications; this was the first for AC bidirectional.

As noted above, UKPN now auto-approves connection applications where the equipment is on the ENA Type Test Register. The other five major DNOs still process applications manually — which means V2G connection timelines vary considerably depending on which network area the installation is in.

For DSO local flex, registration is platform-specific. Piclo Flex, Local Flex, Electron Connect, and Market Gateway each have their own onboarding processes, and there is no single GB registration path. That fragmentation is being addressed in stages: a standardised Prequalification Questionnaire (PQQ) has been rolled out under the ENA Open Networks programme and is now being adopted across all GB DSOs, substantially reducing duplication for providers operating across multiple regions. A Flexibility Market Asset Register — a single registration point for small-scale assets including EV chargers — is planned to launch in 2027.

Gate two: communication — two markets, two different stacks

Once registered, your asset needs to speak the right language to receive dispatch signals. The communication architecture differs completely between NESO-operated markets and DSO flex markets.

For NESO markets, the stack dates back to privatisation and is currently mid-transition. EDT (Electronic Data Transfer) is the FTP/FTPS-based protocol for submitting physical notifications to the Balancing Mechanism. EDL (Electronic Dispatch and Logging) is a separate persistent connection for real-time dispatch instructions to Control Points. Both are being replaced by the OBP (Open Balancing Platform) — the migration window runs through June 2026, documented in NESO’s OBP EDT/EDL Transition Guide V1.2. For new BM entrants, OBP is simply the platform they connect to from day one. The Wider Access API provides a higher-level web interface for participants who do not implement EDT/EDL directly — and is the more practical entry point for most new participants. For non-BM markets — Quick Reserve and Slow Reserve — participants connect via OBP’s SOAP/WSDL web service interface, as specified in NESO’s OBP Web Service Specification v1.3.

For DSO flex markets, the model is different — and simpler for EV operators. There is no equivalent of EDT or EDL. Each DSO procurement platform (Piclo Flex, Local Flex, Electron Connect, Market Gateway) exposes an API through which the aggregator or CPMS receives dispatch instructions, acknowledges them, and reports delivery data back to the DSO. The CPMS then translates those instructions into OCPP smart charging commands sent to the individual chargers. The communication integration point for DSO flex is therefore the CPMS-to-platform API — not a BM-style file transfer or a dedicated real-time control connection.

One note for readers familiar with other markets: IEC 61850, OpenADR 3.0, and IEEE 2030.5/CSIP are not used for NESO or DSO market access in Great Britain. The EU is converging on OpenADR 3.0; the US on IEEE 2030.5. If you encounter these in a V2G context without a jurisdiction qualifier, you are reading about a non-GB deployment.

Gate three: metering — live feeds for NESO, baselines for DSOs

The metering stack is where the majority of EV charging hardware hits a wall it did not know existed — and where the two market types impose fundamentally different requirements.

For NESO BM services — DC, DM, DR, Quick Reserve, Slow Reserve — operational metering is a separate hardware device from the charger. It must deliver active power and state of energy at ±1% accuracy, 1 Hz, reaching NESO’s control room within 5 seconds, as confirmed in NESO’s commissioned operational metering research (DNV, August 2024). For DC and DM, a second layer runs alongside: performance monitoring at 20 Hz — the rate at which NESO verifies that a frequency response was actually delivered. These are two distinct data streams; neither is built into current V2G chargers. Think of it this way: the charger is the worker; the operational meter is the independent auditor who reports directly to NESO every second. You cannot settle a BM contract on the charger’s own data log.

That metering data flows through the iHOST Data Concentrator — NESO’s third-party-hosted platform collecting near-real-time signals from BM and non-BM participants. For small BMUs (under 100 MW, covering all EV aggregations), iHOST connects via IEC 60870-5-104 or MQTT, as documented in NESO’s operational metering guidance (Feb 2026). iHOST and OBP are separate layers: OBP carries dispatch instructions; iHOST carries metering data.

For DSO local flex, the regime is structurally different. No live metering feed to NESO is required. Delivered flexibility is measured against a baseline — the counterfactual consumption profile that would have occurred without the dispatch instruction. As Blake Clough explains, accurate baselining protects both sides: providers are paid for what was delivered; DSOs avoid overpayment. Settlement is monthly, with grace factors and penalisation multipliers creating financial incentives for reliable delivery.

MHHS (Market-Wide Half-Hourly Settlement) tightens the timeline across all markets. Elexon deployed the central systems on 22 September 2025, with meter migration running to May 2027. The settlement lag falls from 14 months to 4 months — a meaningful shift for V2G asset financing.

Gate four: hardware — where physics constrains the ambition

This is the section charger manufacturers need to read carefully.

The question “can this charger do V2G?” is not binary. The more useful question is: which markets can this charger’s hardware, firmware, and connectivity access — and what would need to change to unlock the rest?

What each market actually requires from the hardware and firmware

Every NESO Balancing Mechanism (BM) market — Quick Reserve, Slow Reserve, DC, DM, DR — shares two baseline requirements:

Firmware: OCPP 2.0.1 or 2.1 with full smart charging profiles and ISO 15118-20 for bidirectional power control (ISO 15118-2 for V1G / smart charging only), implemented on both the charger and CPMS (Charge Point Management System — the backend software managing the charger)

Hardware: external operational metering hardware (±1% accuracy, 1 Hz) installed by a qualified metering specialist — a hardware addition no current V2G charger includes.

DSO local flex requires only the protocol layer; G99 approval (Gate one) covers the grid connection.

What separates DC/DM/DR from QR/SR is two additional requirements: 20 Hz performance monitoring alongside the standard metering stream, and sub-second power response: <0.5 seconds to initiate, full delivery within 1 second. The CPMS must also maintain an OBP EDL connection (rather than the SOAP/WSDL interface used for QR/SR) for real-time dispatch. QR/SR has neither of these constraints.

The sub-second requirement is where AC V2G chargers face a fundamental physics problem, not a software problem.

An AC V2G charger — the Zaptec Pro, the Wallbox Quasar 2 in AC mode, any bidirectional AC unit — transfers power through the vehicle’s on-board charger (OBC). The OBC converts AC from the grid to DC for the battery, or DC from the battery to AC for the grid. This conversion cycle operates in the range of tens of milliseconds for a single cycle, but the total system latency — from a frequency deviation event to a grid-side power response — accumulates through the OBC firmware response time, the communication layer, and the power electronics settling time.

ISO 15118-20 Amendment 1, which will likely be published within the coming two months, introduces AC_DER (Distributed Energy Resource) modes, which allow a vehicle to install a droop curve during ISO 15118 session establishment. A droop curve enables autonomous frequency response — the vehicle’s OBC adjusts output power proportionally to frequency deviation, without waiting for an external dispatch signal. In theory, this could bring AC V2G response times within Dynamic Containment’s requirements.

In practice, the AC V2G hardware that works in the UK today — the Zaptec Pro paired with the BYD Dolphin — does not access DC/DM/DR. The Octopus Power Pack operates in DSO-adjacent territory: optimising when to charge and discharge based on grid signals, earning from time-of-use arbitrage and smart charging services, but not submitting to NESO’s Dynamic Containment tender. That is not a criticism of the product; it is an honest description of where the market is.

What a DC V2G charger currently needs

DC V2G takes power from the vehicle battery directly as DC current, bypassing the vehicle’s OBC entirely. The charger’s own bidirectional inverter handles the AC/DC conversion. This removes the OBC latency from the response chain.

The Wallbox Quasar 1 (CHAdeMO, DC V2G) is the charger that makes V2G commercially available to Nissan Leaf, e-NV200, and Mitsubishi Outlander PHEV owners via Octopus Power Pack. The Wallbox Quasar 2 (CCS, ISO 15118-20, DC V2G) supports the Kia EV9’s V2G capability — but is not currently available in the UK.

DC chargers face the same external metering requirement as AC for BM access. More practically limiting: NESO’s BMU registration requires aggregation to 1 MW or above. A single 7.4 kW DC V2G charger cannot register as a BMU alone — an aggregator must bundle many such assets.

The three things that would need to change

Not everything missing from current V2G hardware requires a hardware redesign. It helps to be precise about what kind of change is required:

1. Hardware redesign (firmware cannot fix this): Sub-second frequency response from AC V2G requires power electronics capable of that response envelope — the OBC is the constraint. If ISO 15118-20 Amd. 1 AC_DER droop curves are implemented and validated within Dynamic Containment’s window, some of this could resolve in firmware — but the power electronics must support it.

2. Software changes (firmware-first): Two distinct tasks, two distinct owners. Most V2G chargers today do not fully implement OCPP 2.1 or ISO 15118-20 — a firmware update for the charger manufacturer. Connecting to NESO via the OBP platform is a separate task owned by the CPMS or aggregator, requiring no charger changes.

The exception is a full ISO 15118-20 implementation with Plug & Charge — and shipping ISO 15118-20 without Plug & Charge is a product decision few manufacturers would make. ISO 15118-20 mandates TLS 1.3 and uses secp512r1 as its default elliptic curve — double the key size of the secp256r1 used in ISO 15118-2. Plug & Charge adds mutual TLS authentication: the EV must cryptographically prove its identity to the charger. If the charger’s crypto chip does not support TLS 1.3 cipher suites or the secp512r1 / Curve448 curves (more on that in a previous Plug & Charge article), no firmware update will fix it. Hardware released before ISO 15118-20 was finalised is the most exposed. For those chargers, Plug & Charge may become a hardware replacement question, not a software roadmap item.

3. Protocol replacement (hardware likely needed): CHAdeMO and ISO 15118-20 are incompatible protocol stacks. The Quasar 1’s vehicle compatibility list — Nissan Leaf, e-NV200, Mitsubishi Outlander PHEV — is bounded by that choice; newer V2G-capable vehicles use CCS. As the industry converges on CCS/ISO 15118-20, CHAdeMO-based V2G hardware will need replacing. AFIR mandates ISO 15118-20 for new public DC fast chargers in the EU from 2027; the UK’s Department for Energy Security and Net Zero (DESNZ) is actively consulting on an equivalent UK framework, and the direction of travel is the same. CHAdeMO is a product lifecycle question with a visible countdown.

Gate five: aggregation — the commercial layer most operators outsource

Very few EV operators will interact with NESO or DSO Flex markets directly. The practical route to grid revenue for most fleet operators and CPOs is through an aggregator.

Three terms appear in the same conversations and are not interchangeable:

Flexibility Service Provider (FSP): the entity that owns or controls the assets — a fleet operator with V2G EVs, a CPO with bidirectional chargers. The FSP provides flexibility to the market.

Aggregator: groups multiple FSPs’ assets into a dispatchable portfolio. Can be the same entity as the FSP (a large fleet operator might aggregate its own assets) or a third party. Aggregation is what makes small assets economically viable — a single 7.4 kW charger cannot register as a BMU; 150 of them, aggregated, might.

Virtual Lead Party (VLP): a specific BSC-defined role for parties dispatching assets they do not supply electricity to. This is the formal mechanism that allows an aggregator to participate in NESO markets without being the electricity supplier of record for the customer.

An analogy that holds up better than most: the FSP is the athlete. The aggregator is the sports agency. The VLP accreditation is the agency’s BSC licence — without it, the agency cannot bill for grid services on behalf of athletes it doesn’t also supply power to.

The VLP role became considerably more valuable in November 2024. BSC Modification P415 opened wholesale market access to VLPs directly. Before P415, a VLP could dispatch assets in the Balancing Mechanism but had to route wholesale market participation through an Energy Supplier intermediary — the BSC assigned all customer flexibility to the customer’s Supplier by default. After P415, VLPs can register directly with Elexon as a Virtual Trading Party and access the wholesale market independently.

For V2G aggregators, this matters: wholesale and BM revenues make up approximately 60% of a typical BESS revenue stack — with Capacity Market another ~10% — based on Modo Energy’s benchmark of £73,145/MW/year for two-hour GB batteries over the twelve months to April 2026. No published V2G-specific equivalent exists; BESS is the closest proxy. P415 means an independent V2G aggregator can now capture that wholesale share directly rather than routing it through a supplier.

Active GB aggregators in the EV and flexibility space include:

Octopus Kraken (supplier and aggregator, whose Power Pack tariff is the consumer product),

Flexitricity (now part of Drax, BM participant),

CrowdCharge via GridBeyond (EV-specific aggregator),

Axle Energy (EV aggregator),

AmpVerve (V2G platform focused on the orchestration layer between grid dispatch and settlement), and

Habitat Energy (BESS-focused, increasingly flexible with asset types).

What the aggregator actually takes on and what you need to hand over

The aggregator handles dispatch, verification, and settlement end-to-end. Once onboarded, the CPO does not interact with NESO or the DSO directly; the aggregator does. What the CPO must provide is the data and control surface the aggregator builds on:

Visibility: charger behaviour, transaction status, charger availability, and location, surfaced via the CPMS

Control: the ability to adjust or reduce power output, delay charging, and schedule charging events — delivered through OCPP smart charging profiles

Grid connection evidence: a G99 certificate per individual charger for any market involving energy export

For V2G specifically, the OCPP version matters: OCPP 1.6J or 2.0.1 supports V1G onboarding; OCPP 2.1 and ISO 15118-20 are required for bidirectional dispatch.

Revenue splits are not standardised, but the structure is consistent across most aggregators: the asset owner (CPO or fleet) receives the majority of the grid service revenue — typically 80–90% — with the aggregator retaining the remainder as its service fee. The aggregator’s cut covers the market access, VLP/VTP licences, metering data transmission to NESO or the DSO, and settlement administration. From a CPO’s perspective, the practical output is a grid services revenue line with no direct regulatory exposure — the complexity of BSC registration, OBP connectivity, and metering compliance sits with the aggregator.

Where this leaves fleet operators, CPOs, and charger manufacturers

The announcements keep coming — V2G-capable, bidirectional, vehicle-to-grid ready. The number of UK grid payments any of those vehicles can earn does not. The five gates in this article are what that gap is made of — and several of them are moving: the OBP migration window closes at the end of this month, UKPN’s auto-approval has been live since March, and P415 rewrote independent aggregator economics six months ago. The stack is not waiting for the industry to catch up.

Fleet operators: If you have legacy CHAdeMO vehicles, the Octopus Power Pack / Quasar 1 pathway delivers real grid payments today — but do not extend your CHAdeMO footprint. For new procurement, the standard to build on is CCS with ISO 15118-20 bidirectional capability for passenger and light commercial vehicles; for heavy-duty trucks, MCS (Megawatt Charging System). Both are where the industry is converging; CHAdeMO is not. On the market side: DSO local flex is the most immediately accessible entry point: lower barriers than NESO, no external metering hardware required, and contracted at scale across all six GB distribution regions already. For NESO ancillary services, you need an aggregator with BSC registration and ±1% external metering at your sites. Neither is off-the-shelf, but both are tractable with the right aggregator partner.

CPOs: The communication layer is in transition. If you are connected to NESO markets via the legacy BM system, your Trading Agent must transition to OBP by the end of June 2026. If you use the Wider Access API, NESO manages this for you. For DSO local flex, the relevant platform depends on geography — Piclo Flex, Local Flex, Electron Connect, or Market Gateway, depending on which DSO serves your sites.

Charger manufacturers: Three different kinds of gap exist in current hardware:

a physics constraint (AC response latency for DC/DM/DR),

a firmware gap (OCPP 2.1 and full ISO 15118-20 support, which most V2G chargers today lack), and

a protocol replacement requirement (CHAdeMO to ISO 15118-20 as AFIR approaches).

The first requires an honest engineering assessment of what your OBC can do. The second is firmware-first, but with a hardware caveat: ISO 15118-20 with Plug & Charge requires crypto chip support for TLS 1.3, secp512r1, and Curve448 — hardware that predates the standard may not have it, and no firmware update can add a missing crypto curve the hardware doesn’t support. The third is a product lifecycle question with a visible countdown — AFIR mandates CCS/ISO 15118-20 for new EU public DC fast chargers from 2027, and DESNZ is consulting on the same for the UK. The ENA Type Test Register is the gating database for UK connection approval — if your product is not listed, the gate remains closed.

The next article in this series will cover the economics: what these markets actually pay and how aggregators model the revenue stack.

Enjoyed this deep dive?

Then please share with your professional (social) network

and restack for your readers.

Marc - this is a great article showing all the steps to get to real V2G.

I have a small piece of good news: the BM metering requirements have been relaxed, but it's very understandable that this isn't obvious. I participated in that DNV project you mention, and 1%/1Hz per device is the standard BM metering requirement, but in the project we were able to show that this wasn't necessary for aggregated small assets, and so now the requirement has moved to the aggregate.

This went live in March 26: https://www.neso.energy/news/millions-households-and-businesses-free-reap-rewards-flexing-energy-use. Very little technical detail here I'm afraid, so this article is better: https://utilityweek.co.uk/neso-to-relax-balancing-mechanism-rules-for-aggregated-small-scale-assets/, or wade through the 250+ pages of DNV's report: https://www.neso.energy/document/372636/download.

In short, the requirement is 1% accuracy in the aggregate with a minimum of 30s reads from the asset.

Great article on GB model. EU recently published a SEEG/STF/CoW (?!) https://op.europa.eu/en/publication-detail/-/publication/f56915a6-5582-11f1-b3e2-01aa75ed71a1

On same subject but introduced new actors and objects such as DER Operators, Smart Charging classifications and Energy Transfer Plans. Any comments?