Inside the UK electricity market's four layers

Most EV professionals see one market. There are actually four, each running at a different speed. Here's how they work — and where your fleet fits.

Sometime last winter, a large power station in Great Britain tripped unexpectedly offline. Its output, several hundred megawatts, vanished from the system in seconds. Grid frequency began to fall. Within half a second, battery storage assets across the country began discharging: not because anyone phoned them, not because a control room engineer issued an instruction, but because their power electronics were measuring local grid frequency every second and responding to a curve that had been pre-loaded at commissioning. The response was already embedded in the hardware. No instruction crossed the wire.

If a fleet of V2G-capable EVs had been enrolled and plugged in at that moment, they would have earned revenue on someone’s driveway or even at a public charging station.

The previous articles covered the technical prerequisites: grid codes (G99, EN 50549-1) that define what a bidirectional device must do when frequency deviates; OCPP 2.1 and ISO 15118-20 carry those parameters from a grid operator’s systems to the AC/DC inverter — inside the DC charger for DC, or inside the vehicle’s on-board charger (OBC) for AC. The protocol chain is being assembled. The grid code framework is largely in place.

What we have not covered is the market side: which trading systems those protocols are connecting into, why those markets exist in the forms they do, and where an aggregated EV fleet can actually earn money today versus where it might in the future. That is what this article is about.

In this article, you will learn:

How Great Britain’s (GB) electricity market is structured across four distinct layers — from long-term capacity planning through wholesale trading, real-time balancing, and the frequency response services that react in under a second — and why each layer exists

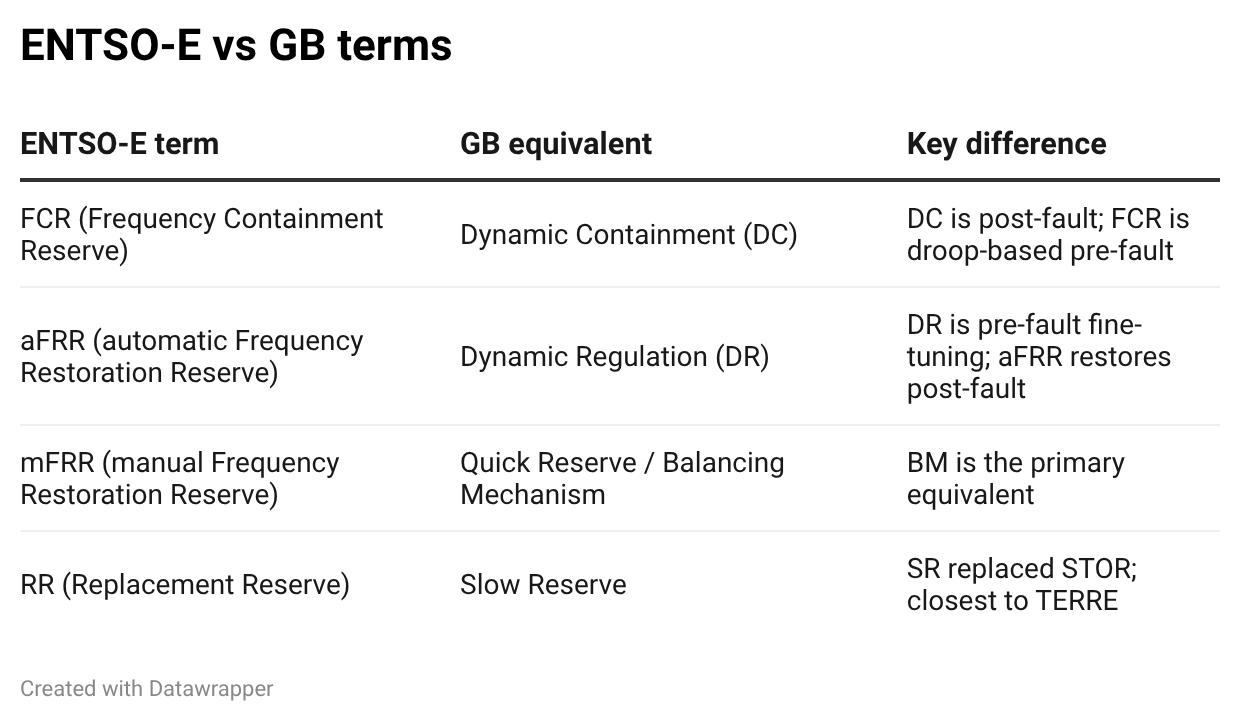

Why GB’s market has its own terminology (Dynamic Containment, Balancing Mechanism, Slow Reserve) that does not map neatly onto the ENTSO-E vocabulary familiar from continental European V2G work

Where an aggregated EV fleet can participate today, what the current barriers are, and which market opening in September 2025 is the most significant recent unlock

Latest articles:

If you haven’t subscribed yet, here’s what was covered in the past weeks:

The four-layer market

Before electricity was privatised in the late 1980s and early 1990s, Great Britain (GB, meaning: England, Wales, and Scotland, excluding Northern Ireland — that’s why I distinguish between GB and the UK in this article) had the Central Electricity Generating Board: a nationalised monopoly that ran generation, transmission, distribution, and supply as a single entity. Infrastructure investment was government-directed; electricity sales were structured to cover costs. Privatisation broke all of this apart. Different companies now generate, transmit, distribute, and supply electricity. Each layer operates under a separate licence from Ofgem (Office of Gas and Electricity Markets), the independent regulator. And the job of coordinating them — making sure supply matches demand at every moment — fell to a system operator.

That system operator is NESO (National Energy System Operator, formerly National Grid ESO until it was rebranded in April 2024). NESO does not own generation assets. It does not sell electricity. Its job is to keep the physical system in balance in real time and to procure the services needed to do so. NESO is structurally neutral on who generates and who supplies; it sees only the physical output, not the commercial arrangements behind it.

Layered on top of the physical system are four distinct markets, each solving a different problem at a different timescale.

The Capacity Market operates years in advance. Its purpose is security of supply: ensuring that enough generation capacity will exist to meet peak demand when it occurs. It pays generators and storage assets for the commitment to be available, not for energy delivered. Power stations and batteries win Capacity Market contracts in annual auctions (T-4, four years ahead; T-1, one year ahead) and receive availability payments in return. For a new-build power station that needs project financing, a fifteen-year Capacity Market contract is often the prerequisite. Without that long-term revenue floor, the merchant market alone does not guarantee the investment.

The Wholesale Market is where electricity is bought and sold. Generators sell what they plan to produce; suppliers buy what they forecast their customers will use. This trading happens across a spectrum of timescales, from futures contracts years ahead of delivery all the way to continuous intraday trading up to one hour before a delivery period. The wholesale price is what most people mean when they talk about “the price of electricity.”

The Balancing Mechanism (BM) is NESO’s real-time correction tool. After a boundary called gate closure — one hour before each half-hour delivery period — participants can no longer trade on the open market. Whatever was agreed in the wholesale market is now locked in. Any remaining gap between what participants said they would generate or consume and what the system actually needs is corrected through the Balancing Mechanism: NESO instructs registered assets to increase or reduce output and pays them accordingly.

Ancillary services are the layer many people in the EV charging industry have not spent much time thinking about, but which matters enormously for Vehicle-to-Grid (V2G). These services handle everything that is too fast, too continuous, or too specialised for the wholesale market and the Balancing Mechanism to manage: frequency stability, voltage management, system inertia, and the ability to restart the grid from a complete shutdown. This is where battery storage has built its GB business model, and where V2G has the most technically demanding but commercially significant opportunity.

The UK’s market administration involves three key bodies beyond NESO itself. Ofgem sets the rules and issues licences; participants must hold the correct licence before operating. Elexon administers the Balancing and Settlement Code (BSC), the legal and technical framework that governs the BM and the settlement of imbalances: a document that runs to over a thousand pages and underpins every commercial transaction in the BM. DNOs (Distribution Network Operators) manage the physical local distribution network — the cables and substations that deliver electricity to homes and businesses — and are increasingly procuring local flexibility services from batteries and flexible demand in their areas.

Wholesale markets: where electricity gets a price

The Great Britain electricity market uses a twenty-four-hour trading day that does not start at midnight. It runs from 23:00 one night to 23:00 the following night, divided into six four-hour EFA (Electricity Forward Agreement) blocks. Block 1 is 23:00–03:00; Block 6 is 19:00–23:00. The settlement periods that determine final financial positions run midnight to midnight in forty-eight half-hour slots — so the first two settlement periods of any EFA day are actually buried in the previous calendar day’s settlement register.

day. Source: The Energy Academy - Modo Energy")

Electricity is traded across three main timescales.

Forward and futures markets operate years ahead of delivery. A generator might sell its expected output across a whole calendar month — a baseload product covering all six EFA blocks — locking in a price and removing exposure to short-term price swings. Futures are standardised contracts traded on an exchange (primarily Intercontinental Exchange, or ICE); forward contracts are bilateral, negotiated between a generator and a supplier. These long-horizon trades give both sides certainty and let them hedge risk.

Day-ahead trading happens, as the name suggests, the day before delivery. GB’s main day-ahead exchanges are N2EX (operated by Nasdaq/NordPool) and EPEX Spot. These run single-price auctions: all accepted participants receive the same clearing price. The day-ahead price is the most widely quoted electricity price signal in GB.

Intraday trading is continuous, from day-ahead close up to gate closure one hour before delivery. Participants buy and sell as demand forecasts update and generation availability changes. The exchanges also run half-hourly auctions within the continuous session, allowing very granular positioning close to real time.

What sets the wholesale price? The answer is the merit order: a ranking of all available generation by short-run marginal cost, starting with the cheapest (typically zero-marginal-cost wind and solar) and working up to the most expensive (typically gas peaking plants).

Short-run marginal cost: The cost of generating one additional megawatt-hour right now — fuel, variable operations and maintenance, carbon tax costs — but not the capital cost of building the plant (that’s already sunk). A gas turbine burning expensive gas has a high SRMC. A wind farm with no fuel has a SRMC near zero. This is why wind and solar, once built, always run: they cost almost nothing to operate, so they always sit at the front of the merit order.

Electricity is a commodity that must be balanced in real time, so the system prices at the marginal cost of the most expensive unit needed to meet demand at that moment. On a day of high wind and low demand, the marginal unit might be an efficient gas plant ticking over at part load — cheap to run, setting a low price. On a still winter evening, when cheaper generation is already running flat out, it might be a gas peaker: a plant that sits idle most of the year and only switches on when demand exceeds everything else in the stack, at a significantly higher cost. Every generator that ran in that period, regardless of its actual costs, receives that marginal price.

For a battery storage asset or an EV fleet aggregator, this creates an opportunity: buy when the merit order is being cleared by cheap renewables (prices are low or even negative), sell when expensive gas sets the marginal price (prices are high). The spread between these two is the arbitrage value. In 2024, there were 176 hours of negative wholesale pricing in GB (Modo Energy) — electricity so abundant that generators were paying to push it onto the system. Those are the charging windows for EVs.

Small distributed assets cannot access wholesale markets directly. The administrative overhead, minimum lot sizes, and settlement complexity are built for large industrial participants. A fleet aggregator accesses these markets on behalf of its clients, taking on the settlement, the metering obligations, and the market participation risk. We’ll cover examples of fleet aggregators in one of the next articles.

The Balancing Mechanism: correcting the gap

At gate closure, one hour before each settlement period, the market freezes. Every registered participant — every generator, every large consumer, every battery storage site — submits its Final Physical Notification (FPN): its locked-in plan for what it will generate or consume in that half-hour. These FPNs are the map of what the physical system expects to look like.

The map is never quite right. A wind farm produces more than forecast. A large industrial site shuts down unexpectedly. A power station experiences a partial outage. The total generation and total demand in NESO’s forward picture do not balance.

The Balancing Mechanism handles this gap. Registered participants (Balancing Mechanism Units, or BMUs) submit two prices alongside their FPNs: a bid price — the cost at which they will flex down (reduce generation or increase demand) — and an offer price — the cost at which they will flex up (increase generation or reduce demand). NESO sorts all available bids and offers by price and accepts the cheapest combination that balances the system. When it accepts an offer (instructing a BMU to generate more), it issues a Bid Offer Acceptance (BOA) and pays the offer price. When it accepts a bid, it pays the bid price.

Participants that deliver differently from their FPN and BOA commitments face imbalance pricing, administered by Elexon. Under-generate relative to your commitment, and you must buy the shortfall at the System Buy Price. Over-generate relative to your commitment, and you sell the excess at the System Sell Price. Both prices reflect the actual cost NESO incurred to balance the system in that period. The financial incentive is clear: match your FPN as precisely as possible, and avoid the System Price. Getting it wrong is expensive.

One significant development in December 2023 was the launch of NESO’s Open Balancing Platform (OBP). The older system required BM registration through Elexon to access most balancing services — a significant barrier for small, distributed assets. OBP began changing this. From September 2025, non-BM units can access Quick Reserve (a one-minute response service) via OBP. Dynamic Response services opened to non-BM units in January 2026; Slow Reserve followed in March 2026. The BM is no longer the only door into these markets.

And here is the structural insight the BM reveals about ancillary services: the Balancing Mechanism is fundamentally an instruction-based, commercial market. NESO issues a BOA, the BMU responds. The fastest this loop can physically complete — with network latency, control room processing, and plant response time — is measured in minutes. The Balancing Mechanism is an effective tool for correcting the gap between the scheduled position and what the system needs over a half-hour period.

It cannot fix frequency in the next 500 milliseconds.

Frequency services: faster than any instruction can travel

At any given moment, GB’s electricity system runs at 50 Hz. Frequency is not a target that NESO actively pushes toward — it is a physical emergent property of the balance between generation and demand. When generation exceeds demand, rotational inertia in synchronised turbines speeds up, and frequency rises. When demand exceeds generation, inertia slows, and frequency falls. 50 Hz means the system is balanced.

NESO must keep frequency within operational limits (±0.2 Hz, so 49.8–50.2 Hz under normal conditions) and must never allow it to breach statutory limits (±0.5 Hz, so 49.5–50.5 Hz). Significant deviations damage equipment and, at their extreme, trigger automatic disconnection of generators and loads — the cascade that leads to a blackout.

The problem is physics. When a large generator trips offline, frequency begins falling within milliseconds. Any response that depends on an instruction from NESO — receiving a BOA, having a plant operator respond, ramping up generation — takes minutes to complete. By that point, frequency may have already breached the statutory limit.

The solution is pre-positioned, autonomous response: assets that monitor local frequency continuously and respond without waiting for any instruction from anyone.

GB procures three Dynamic Response Services for this purpose, all launched from 2020 onwards as part of a major refresh of the ancillary services framework.

Dynamic Containment (DC) is the post-fault service: it activates after a frequency deviation has already occurred. DC assets respond within 0.5 seconds of the deviation appearing, reaching full contracted capacity within 1 second and sustaining that response for up to 15 minutes. DC-Low handles under-frequency events (a generation loss, where the asset discharges to inject power); DC-High handles over-frequency (a demand loss or surplus renewable generation, where the asset charges to absorb excess).

DC is procured in daily auctions, cleared per EFA block, on a pay-as-clear basis. The clearing price is volatile: it can exceed £60 per MW per hour during periods when NESO is competing hard for DC capacity. According to its Annual Balancing Services Spend Report, NESO spent £92 million on Dynamic Response Services in 2024–25.

Pay-as-clear auctions: NESO ranks all bids from cheapest to most expensive and accepts enough to reach its volume target. The clearing price is set by the most expensive bid needed to fill the requirement — and every accepted bidder receives that price, not their own bid. The alternative, pay-as-bid, encourages gaming (bidding just below where you expect clearing to be). Pay-as-clear removes that incentive. Older services like Firm Frequency Response (FFR) used pay-as-bid; DC does not.

Why does battery storage dominate the DC market?

Because no other technology can reliably deliver sub-second response. A gas turbine needs minutes to ramp. Wind turbines connect to the grid through power electronics rather than being directly coupled to AC frequency, so they do not contribute the synchronous inertia that slows frequency change. Batteries respond in milliseconds. In LocalFrequency mode under OCPP 2.1 — the protocol mechanism described in one of my previous articles — a charging station reads local grid frequency and adjusts its power output autonomously using a pre-configured frequency-power droop curve. No NESO instruction required. No round-trip delay. The response is already there.

Dynamic Moderation (DM) is a pre-fault service: it activates not because a fault has occurred, but because the system is behaving in a particularly volatile way — gusting wind causing rapid generation swings, for instance. DM assets maintain the same sub-second response capability as DC assets but are held in reserve to dampen pre-fault frequency volatility before it can develop into a fault event.

Dynamic Regulation (DR) is also pre-fault, but slower: 2 seconds to initiation, 10 seconds to full delivery, sustained for up to 60 minutes. DR is the continuous fine-tuning layer — the service that keeps frequency close to 50 Hz during normal system operation, correcting the small deviations that occur constantly throughout the day. In ENTSO-E terminology, DR is the closest equivalent to aFRR (automatic Frequency Restoration Reserve), though the operational role differs: aFRR restores frequency after a fault; DR prevents deviations from growing before they become faults.

Alongside DC, DM, and DR, two reserve services bridge the gap between the sub-second frequency response layer and the minutes-long Balancing Mechanism. Quick Reserve (QR) delivers within one minute of an instruction and must be capable of sustaining output for at least five minutes. Slow Reserve (which replaced STOR, the Short-Term Operating Reserve, when it retired on 1 April 2026) delivers within fifteen minutes. Both services are now accessible to non-BM units through OBP.

The terminology that matters when you are reading ENTSO-E literature alongside GB material:

The Capacity Market rounds out the financial architecture. For battery storage assets — and eventually for V2G aggregators — it provides a long-term availability payment: roughly £7,454 per MW per year for a typical 2-hour battery asset in the twelve months to April 2026 (Source: Modo Energy GB BESS Revenue Benchmark, H1 2025), representing about 10% of total revenue. The Capacity Market does not pay for energy delivered; it pays for the commitment to be available. The duration problem is real: a battery must demonstrate it can sustain output for a minimum period during a stress event, and the de-rating factors applied to short-duration storage are significant.

A four-hour battery achieves a 44% capacity credit; an eight-hour battery achieves 92%. An EV fleet faces a compounding version of this problem: the Capacity Market’s duration requirements assume firm, predictable availability, and a fleet whose plug-in hours depend on driver behaviour cannot reliably commit to that. Capacity Market participation is rather a long-term prospect for EV aggregators, not a near-term revenue stream.

Where EVs fit today, and where they’re going

The honest answer about where aggregated EVs sit in the GB grid market in 2026 is: at the beginning of a journey that the industry has now demonstrably started.

The starting point is the Powerloop trial, run by Octopus Energy Group in collaboration with NESO in 2022. Up to twenty electric vehicles were linked directly to NESO’s Electricity National Control Centre — the first time residential V2G assets had been connected to the Balancing Market in Great Britain. The demonstration proved that a domestic EV could receive grid signals and adjust its charging and discharging in response. The potential annual savings for a participating driver were modelled at up to £840 per year versus a flat-rate tariff, for a driver travelling 10,000 miles annually (Sources: NESO Powerloop trial report; Octopus Energy press release, August 2022).

But the trial also surfaced a hardware limitation that defines the state of the art: the V2G charge points used in Powerloop measured active power only every ten seconds, with a ±8% margin of error. Dynamic Containment requires 1 Hz metering and sub-second response. The 2022 trial demonstrated BM eligibility in principle; it did not demonstrate DC participation. The fastest frequency response markets remain out of reach for current V2G hardware — not because of market rules, but because of metering and response-time specifications that most chargers have not yet been built to meet.

Three years on, the market has moved in two important directions.

Smart charging at scale. The CrowdFlex trial, the UK’s largest home energy flexibility programme, ran from May 2024 to September 2025. Led by NESO and funded by Ofgem’s Strategic Innovation Fund, it tested whether domestic EV charging could be aggregated and dispatched as a flexibility resource. 33,000 customers participated in the Summer 2025 EV availability trials through Ohme and OVO’s smart charging platforms (Source: NESO CrowdFlex project, NESO CrowdFlex: Full Programme Executive Summary). Ohme’s EV drivers were collectively rewarded with £750,000. CrowdFlex was smart charging — V1G, meaning it managed when and how fast EVs charged, without any bidirectional discharge. But it proved the aggregation infrastructure at a scale that matters for V2G planning.

The first commercial V2G bundle. In June 2025, Octopus Energy, BYD, and Zaptec launched the UK’s first commercial vehicle-to-grid product: the Power Pack. Customers lease a BYD Dolphin EV and receive a Zaptec Pro bidirectional charger with free home charging included. Octopus’s Kraken platform manages charging and discharging automatically — plugging in for at least twelve hours a day on average and staying within 210 kWh monthly consumption qualifies the customer for the free charging benefit. Independent modelling by Gridcog estimates Octopus could generate £526 to £1,015 per vehicle per year depending on market participation — excluding charger hardware costs and the portfolio benefit from managing imbalance positions, which Gridcog notes is likely to be material. The customer’s benefit is delivered as free charging rather than a direct cash payment — roughly £620 in annual savings compared to a standard variable tariff.

The Power Pack is currently focused on wholesale price arbitrage: charge when electricity is cheap (during high-wind, low-demand periods), export when prices are high (during evening peak). It is the accessible, commercially straightforward entry point into the V2G market. Frequency response participation at the DC/DM/DR level is not confirmed for the product as it stands — which points to the metering and hardware requirements that the Powerloop trial identified.

The Open Balancing Platform (OBP) unlock. The most significant structural change for EV aggregators in the last twelve months is the opening of non-BM access to reserve services via OBP. Quick Reserve — the one-minute response service — became accessible to non-BM units in September 2025. Slow Reserve followed in March 2026. For an EV fleet aggregator whose vehicles can sustain a managed discharge for one to fifteen minutes under central dispatch, these are realistic markets today. The registration requirements are different from BM registration (and the next article of this series will cover the specifics), but the market door is now open.

The numbers NESO is planning around. NESO estimates that smart charging alone — optimising when EVs charge, without any bidirectional discharge — could shift peak demand by 13 GW by 2035. Adding V2G bidirectional capability could shift an additional 14 GW of demand into off-peak periods (Source: NESO Future Energy Scenarios 2025 — 2035 Key Challenges) — a combined 27 GW of flexible resource from the vehicle fleet alone, within a decade. With 27 million EVs projected on GB roads by 2035, up from fewer than 500,000 today, that flexibility resource grows every year a new EV is sold. A partially aggregated EV fleet by the mid-2030s is not a marginal flexibility resource — it is a system-scale one.

The aggregator is the entity that bridges an individual EV and these markets. It pools vehicles, handles the metering, takes on the market access obligations, dispatches the fleet in response to price signals or NESO instructions, and shares the revenue with participants. What that registration and dispatch process actually requires — the G99 compliance stack, the Balancing Settlement Code (BSC) obligations, the OCPP 2.1 control chain from Kraken to charger to EV — is the subject of the next article.

The GB electricity market is not simple. It is four interlocking mechanisms operating at different timescales, procured through separate platforms, governed by separate codes, administered by separate bodies. Wholesale trading gives electricity a price. The Balancing Mechanism corrects what the market cannot predict. Frequency response services protect the system at speeds the market cannot reach. The Capacity Market ensures the infrastructure for all of this gets built in the first place.

Each layer exists because the one below it cannot cover its ground. That is the key insight for anyone trying to understand why the market has the shape it does. And it is the insight that explains which layers an EV fleet can access, in what order, and at what level of technical sophistication.

The Power Pack launched in June 2025. CrowdFlex ran to September 2025 with 33,000 EV customers. OBP opened Quick Reserve to non-BM units the same month. The market is moving. The question is now what it takes to join it — stay tuned to the next article to find out.

Enjoyed this deep dive?

Then please share with your professional (social) network

and restack for your readers.